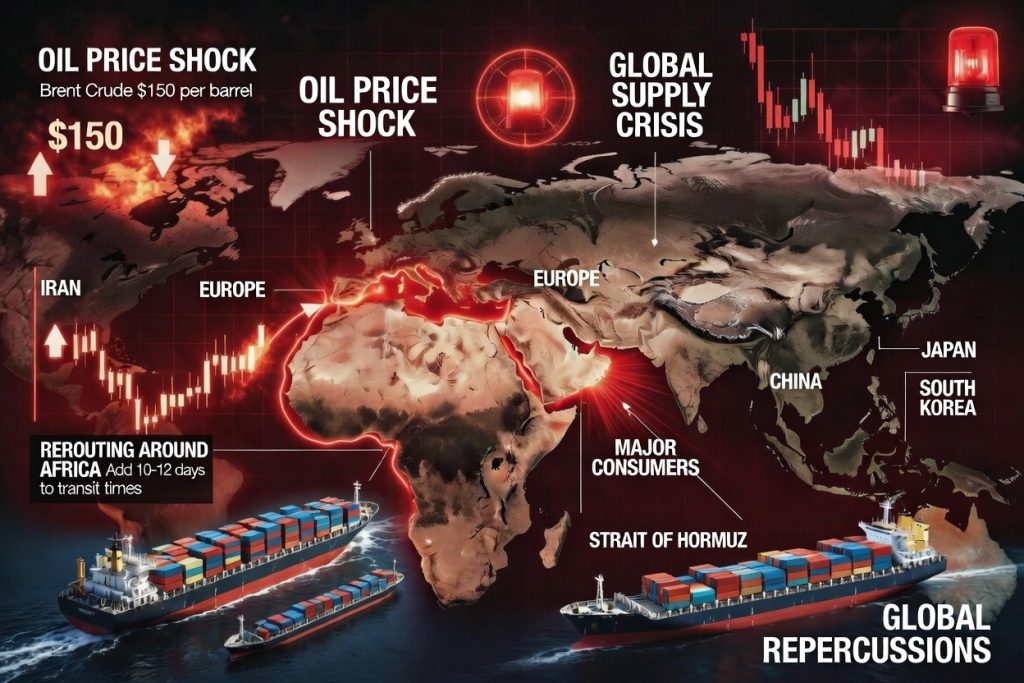

In a dramatic escalation following US and Israeli strikes on Iran, Tehran’s effective closure of the Strait of Hormuz has brought the world’s most critical energy chokepoint to a standstill. This narrow waterway carries roughly 20 million barrels of oil per day—about 20% of global consumption—and a massive share of LNG exports, making it the artery that powers Asia, Europe, and beyond.

Within days, Brent crude has already spiked toward $80–$100 per barrel, with analysts warning of $120–$200+ in a prolonged shutdown. The fallout is immediate and brutal: surging fuel prices, higher shipping costs (with transit times extended 10–12 days), exploding insurance premiums, and the very real threat of stagflation as inflation climbs while growth stalls. Asian giants like China, India, Japan, and South Korea—taking 85% of the oil—face the hardest hit, while Europe scrambles for alternative LNG and developing nations like Pakistan and Bangladesh watch power and transport costs soar. Even distant economies (Mexico’s oil revenues and freight sectors are already reeling) feel the pain.

This is no ordinary supply glitch. A closure of this scale could dwarf the 1970s oil crises and reshape global trade, inflation, currencies, and geopolitics for months or years. In this blog, we break down exactly who wins, who loses, and what governments and businesses must do to survive the Hormuz shockwave.

How a Strait of Hormuz Closure Would Impact Pakistan

Pakistan stands among the countries most vulnerable to a prolonged closure of the Strait of Hormuz, given its near-total dependence on Gulf-sourced energy imports that transit this critical chokepoint. As an energy-importing nation with limited domestic production and fragile foreign exchange reserves, the effects could cascade quickly through the economy, exacerbating inflation, straining the balance of payments, and threatening industrial and household activity.

Energy Supply and Security Risks

- Oil Imports — Pakistan imports roughly 80–90% of its crude oil and a significant portion of refined products (like diesel and petrol) from Middle Eastern countries such as Saudi Arabia, the UAE, Kuwait, and Abu Dhabi. About 80% of crude imports transit the Strait of Hormuz. With domestic production low (around 70,000 barrels per day against demand of ~300,000+), disruptions could lead to immediate supply bottlenecks. Two tankers bound for Pakistan are already reported stuck, and major shipping lines have paused voyages. Current fuel stocks (petrol, diesel) stand at about 28–30 days, buying short-term time but not much beyond that if rerouting fails.

- LNG Imports — Qatar and the UAE supply ~99% of Pakistan’s liquefied natural gas (LNG), all routed through the Strait. Qatar’s facilities have faced hits, and exports are disrupted. Pakistan relies on LNG for power generation and industry; shortages could force load-shedding, cut gas to industrial users (already starting in some cases), and spike electricity costs.

- Alternative Routes — The government is urgently seeking reroutes, including Saudi crude via the Red Sea port of Yanbu (one vessel already arranged). Imports from Fujairah (UAE) or Red Sea sources could help, but these are limited in volume, costlier due to longer distances, and face higher insurance/war-risk premiums.

Economic and Inflationary Fallout

- Oil Price Surge — Global Brent crude has already climbed toward $80–$100+ per barrel amid the crisis. For Pakistan, every $10 rise in oil prices widens the current account deficit by $1.5–$2 billion annually. A sustained $100+ level could add $5–$7 billion to the deficit yearly, potentially wiping out recent surpluses and pressuring the Pakistani rupee further.

- Inflation and Consumer Impact — Higher global prices, plus elevated freight, insurance, and delays, would feed directly into domestic fuel costs. The government has decided to pass on increases via fortnightly adjustments (avoiding subsidies to prevent fiscal blowout), meaning petrol/diesel hikes of Rs 8+ per liter are already anticipated, with more to follow. This drives up transport, food, and manufacturing costs—hitting households hard in an economy already battling inflation.

- Broader Ripple Effects —

- Trade and Industry — Shipping suspensions raise freight charges and slow exports/imports, hurting Karachi port activity and the trade deficit (~$25 billion recently).

- Power and Manufacturing — Gas cuts to industry reduce output; power shortages worsen load-shedding.

- Fiscal Strain — Larger import bills erode reserves; IMF program compliance becomes tougher amid higher subsidies pressure or inflation.

In short, while global markets feel the shock through prices, Pakistan faces both a price shock and a potential physical supply crunch. A short disruption (weeks) strains reserves and budgets; a prolonged one (months) risks energy shortages, stagflation, and setbacks to fragile recovery. The government has formed high-level committees for daily monitoring and is exploring all alternatives—but the Strait’s centrality leaves little buffer.

This scenario underscores why energy diversification (more renewables, strategic reserves, alternative suppliers) remains urgent for Pakistan’s long-term resilience.